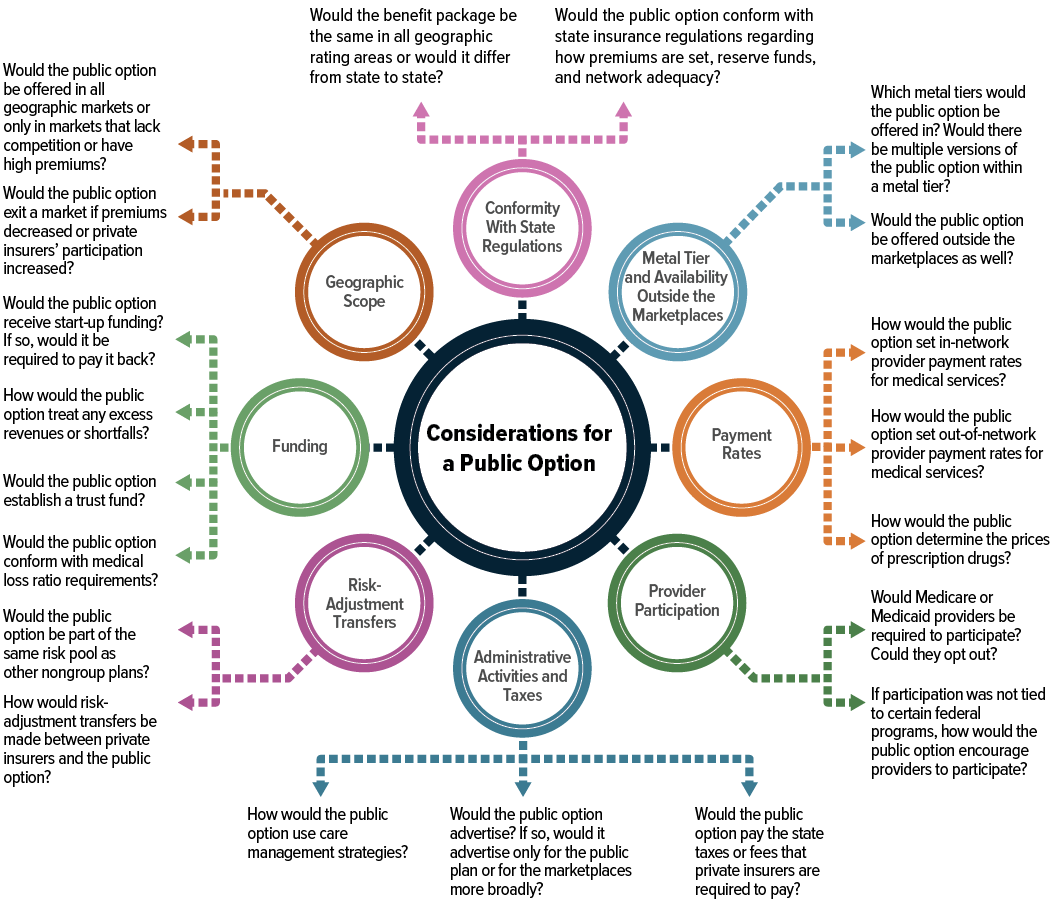

My thoughts on some of the questions, for whatever it's worth.

Care management strategies - I'm not seeing why they wouldn't, mainly for the purpose of being judicious about the provision of cost-effective care.

Would a public option advertise? I don't think there would be a lot of need for that. If some small degree of it is necessary to encourage people to remember there's a marketplace, subsidies, etc. rather than just going direct and paying full price, well okay, but I don't see much benefit in a public option competing for ad space to promote itself. If people go to the marketplace, the prices and benefits will speak for themselves.

Would a public option pay taxes/fees? I don't see the point in governments taxing governments, least of all the federal government being taxable by states.

How would providers be encouraged to participate if not tied to federal programs? Well, through competitive fees for services, right? Coverage should be comparable to what the non-public plans out there are paying, otherwise providers will opt out if at all possible, which they do with Medicare and Medicaid in some cases already.

How would the PO set rates? Depends what the goal is. More generous rates makes establishing a broad participating provider network easy, but then the PO becomes more expensive to the consumer (which the public would find irksome, i.e. they'd ask what's the point of a PO if it's more expensive), or if public funding subsidizes this extra cost it makes better coverage cheaper than it could reasonably be for the non-PO carriers, maybe even leading to some adverse selection into the PO and undermining the real competitiveness of the marketplaces.

What metal tiers would the PO be offered in? Also depends what the goal is. I don't know why it wouldn't be offered across the metal tiers. The way I calculate plans out, it looks to me like the only reason a person should ever choose a Gold plan is if they know they'll hit the OOP maximum every year and would rather pay that cost spread out throughout the year via premiums than in cost-sharing. I've never been able to calculate any other advantage to Gold plans. And with Silver, unless a person's subsidy is more than the cost of the bronze plans, and/or they qualify for CSRs that only apply to the Silver tier, there's little reason to choose Silver either, compared to Bronze. Not sure if that pricing has any relevance to whether a PO should or shouldn't be offered across tiers, but that's my attitude of the tiers and how subsidies affects them. So maybe one thought is just offer the PO in the bronze tier, to try to get people thinking rationally about pricing and the benefits of HDHPs and HSAs, to reduce people's tendency to voluntarily pay more overall for the psychological satisfaction of a small deductible. But, unfortunately there are still a ton of people who see a high deductible and automatically regard it as "crap" coverage, so this would be a strike against its popularity right out of the gate.

Would the PO conform to state regulations? Well there's an awkwardness to the federal government having to follow state rules, but again it would seem that if the PO doesn't attempt to make its plans comparable in most ways to the others in the marketplace, it could eventually undermine the marketplace's functioning/competitiveness. So I would think the PO should aim to be comparable and more or less closely compliant with what the other plans face in a given area.

...

www.cbo.gov

www.cbo.gov