- Joined

- Aug 10, 2013

- Messages

- 20,231

- Reaction score

- 21,633

- Location

- Cambridge, MA

- Gender

- Male

- Political Leaning

- Slightly Liberal

KFF takes a crack at this question today.

The link below is worth following, as they've got some very helpful Tableau graphics embedded in the page that allow you to run different scenarios for folks of different ages and incomes. But I've thrown in some snips below as examples.

One word of caution is that these calculations may understate the savings because they assume Biden revises the ACA's income-based premium caps based on the House Dem's H.R. 1884, which was proposed in this session. Except that the House Dems actually passed a different bill, H.R. 1425, this year that provides for even lower caps than that, meaning more generous subsidies. Unclear why KFF used the former instead of the latter in making these graphics. Other than that, they're excellent.

Affordability in the ACA Marketplace Under a Proposal Like Joe Biden's Health Plan

The link below is worth following, as they've got some very helpful Tableau graphics embedded in the page that allow you to run different scenarios for folks of different ages and incomes. But I've thrown in some snips below as examples.

One word of caution is that these calculations may understate the savings because they assume Biden revises the ACA's income-based premium caps based on the House Dem's H.R. 1884, which was proposed in this session. Except that the House Dems actually passed a different bill, H.R. 1425, this year that provides for even lower caps than that, meaning more generous subsidies. Unclear why KFF used the former instead of the latter in making these graphics. Other than that, they're excellent.

Affordability in the ACA Marketplace Under a Proposal Like Joe Biden's Health Plan

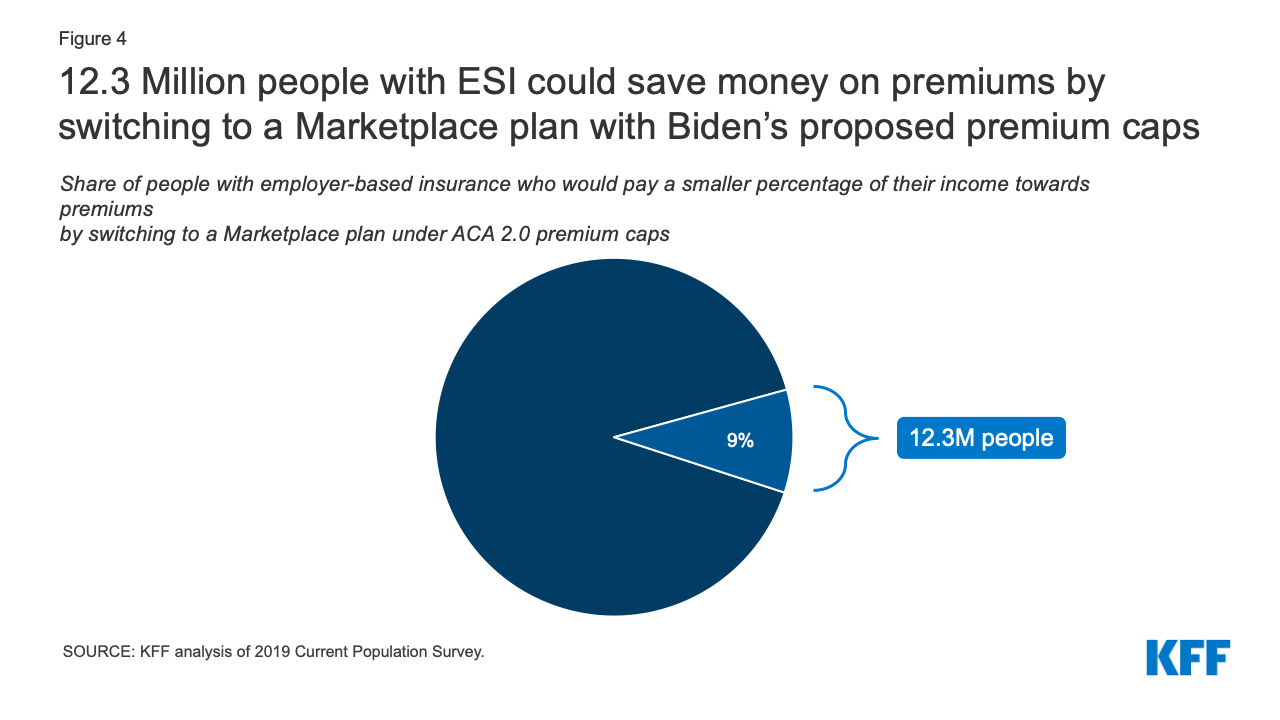

In this portion of the analysis, we focus on the effects of Joe Biden’s health plan on people who are currently purchasing their own coverage, or who would be purchasing this coverage but have been priced out. Biden has proposed building on the ACA by increasing the amount of financial assistance and expanding subsidy eligibility beyond the current range of 100-400% of poverty for Marketplace purchasers. In his plan, Biden would peg the benchmark for premium tax credits to the second-lowest cost gold plan instead of the current silver benchmark, meaning premium subsidies would be higher and Marketplace purchasers could more easily afford a lower-deductible plan.

Biden would reduce the maximum premium contribution cap to 8.5% of an enrollee’s income for a benchmark gold plan (currently the cap on enrollees’ contributions toward the benchmark silver plan is just under 10% of income). He would also remove the upper income limit on premium subsidies, extending the new 8.5% premium cap to higher-income enrollees, and so eliminating the “subsidy cliff.”

")