Dont know about any of that, unrelated:

Lets say I had $50K buried in a hole somewhere.

I dont want to keep losing money on it every year through inflation and COL, and am pretty much completely ignorant of stocks.

What would be my best approach to getting some of this money invested so its growing instead of shrinking?

Maybe a mutual fund?

What about these online robo-brokers? Seems that would be as good a way to invest as any. Seems like fees and stuff could eat into you.

How about some kind of a 401K setup?

I know I could get a book about this and read it (and I will), but any quick tips as to one thing in particular I should really be looking at?

In regards to your OP....do you feel some sort of big correction is coming?

Seems like they prop it up no matter what happens. I know its not "money in the bank" as far as being 100% secure, but still seems like the markets always make out eventually regardless of what happens to the economy in general.

Thanks.

TDameritrade and Schwab were forced a year ago to reduce their $10 fee per buy or sell transaction to zero because Robinhood had gained

a huge number of accounts very quickly by heavily promoting its "no fee" service that depends on selling order flow to market makers who

make and share a tiny margin via "price improvement". Example, the Level II realtime trade activity display shows a bid price of $50 per share and an ask price of $50.11. The client inputs an online trade on Robinhood's website or phone APP, entering a limit order at $50.06 for say... 80 shares. Robinhood routes the order to a market maker offering a .05 percent share kickback. The market maker quickly consolidates the 80 share order into a thousand share order of one of its other clients and executes a buy on an institutional trading platform, buying the 1,000

shares @ $49.85. It doesn't happen that way all of the time, but apparently often enough to remove trading fees from the major competing services like the two I named.

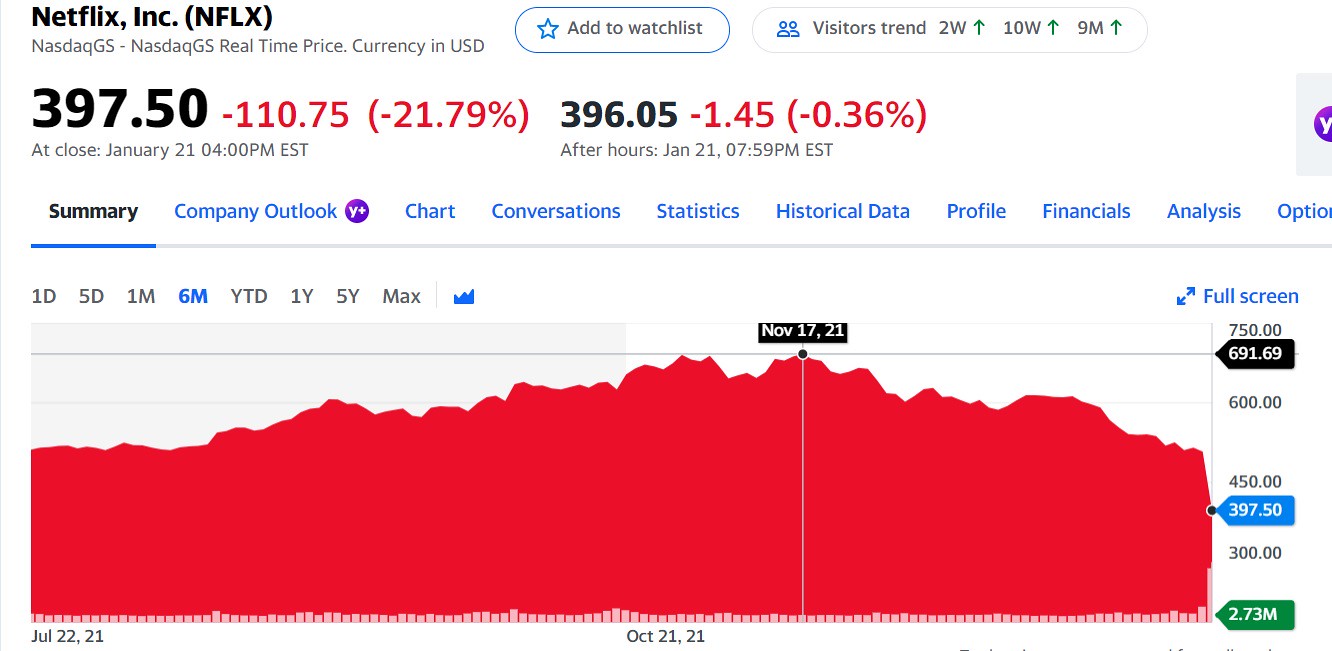

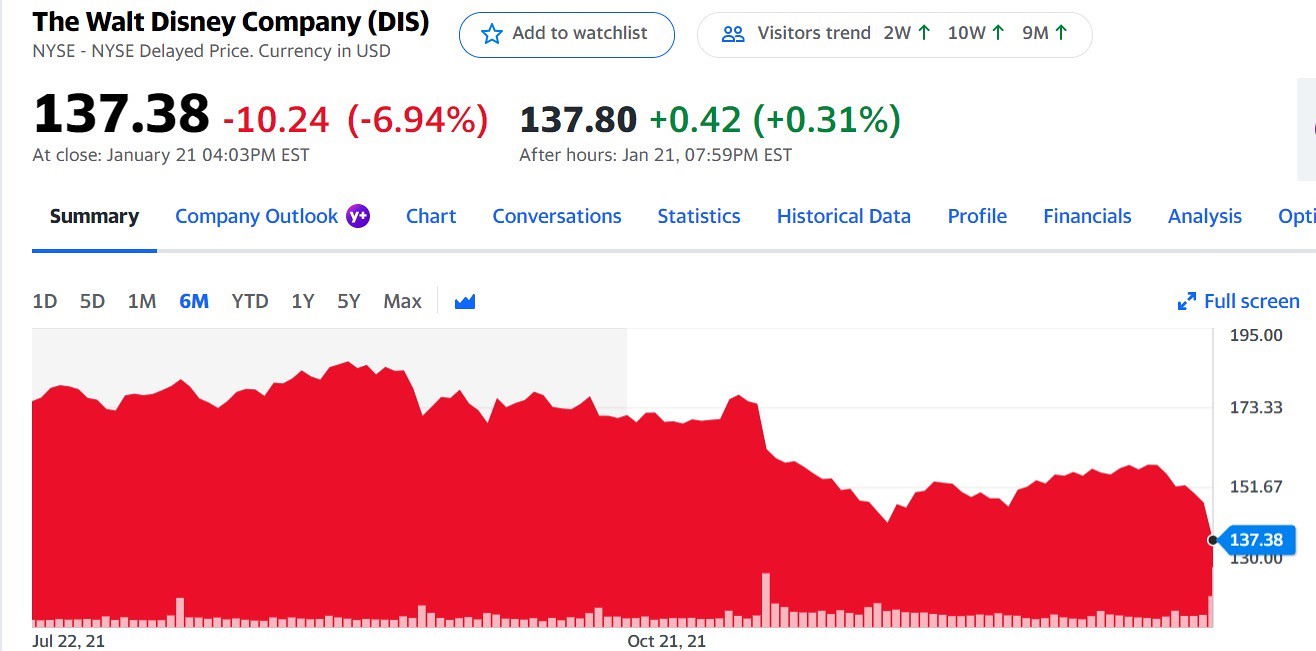

The bad news is HOOD, aka Robinhood, opened it's IPO at a trading price of $38 at the end of last July.

Find the latest Robinhood Markets, Inc. (HOOD) stock quote, history, news and other vital information to help you with your stock trading and investing.

finance.yahoo.com

Robinhood closed at $34.89 that first day it traded and was considered a "busted IPO," a rare thing. However, on

August 4, less than a week later, it touched above $70, dropped to $51 within a couple of days, bounced back to $57 on August 9,

declined steadily since, click the link, above, hit a new low 2 days ago @ $12.77, and last after hours trade on Friday was $12.85 !

Now,,,, they are the broker, if that is the price performance of their own corp.'s stock, what do they have to offer you.

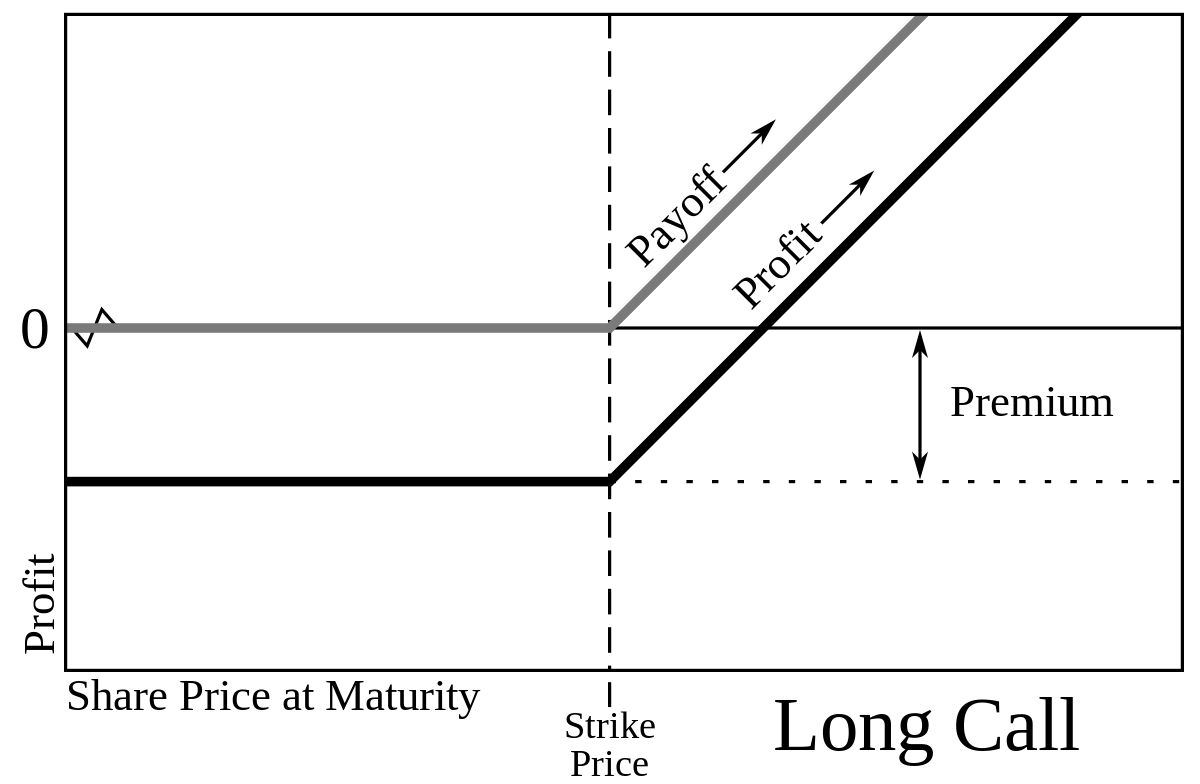

Don't, especially as a novice, buy or short sell a stock or an option in this market through an online broker using any money

you cannot afford to lose.

Ideally, you want to choose a fiduciary, like Fisher Investments. You may have seen their Ads on TV. They are restricted to only selling

you investments that are best for you and they only charge fees on your gains, vs non-fiduciaries that only have to sell you what is

reasonably suited for you but a better profit potential for them than what Fisher is limited to selecting for you, and they can charge fees

regardless of your gains or losses.

The bad news is Fisher requires $500,000 minimum opening investment. I inherited an investment advisor upon the death of my father

a few years ago. He is an Edward Jones partner, as are his 13,000 associates. My dad invested no more than $300,000 when this advisor

was new to that business after leaving a career as a military officer. Edward Jones partners own the company. Each manages an office limited to

about 200 clients. They charge a competitive fee for everything and are not fiduciaries but have a good reputation. He told me he accepted my

father as a client more than 20 years ago but currently requires a $2 million minimum of new clients. He considers me a legacy account and unfortunately most of my Dad's equity was spent on his four years in a long term care facility. You can't qualify for medicaid assistance until you are broke! So, my Edward Jones financial advisor will handle any amount I choose to invest in either a retirement IRA, tax deferred, or a regular investment account and the strategy of that firm, investing and hedging against losses like in this current market

permits them to offer an expectation of a consistent 5 percent return annually!

So, it's nice to know Edward Jones is there if I need its services but I do have 24 years experience trading stocks but more often,

options. As you can see, I started this poll thread because I do not have a high enough confidence about what to do, tomorrow morning!

Smart people with $2 million, are known to settle for a nearly guaranteed 5 percent annual return, hopefully after Edward Jones deducts its

fees.

Continued....