- Joined

- Aug 10, 2013

- Messages

- 25,754

- Reaction score

- 33,003

- Location

- Cambridge, MA

- Gender

- Male

- Political Leaning

- Slightly Liberal

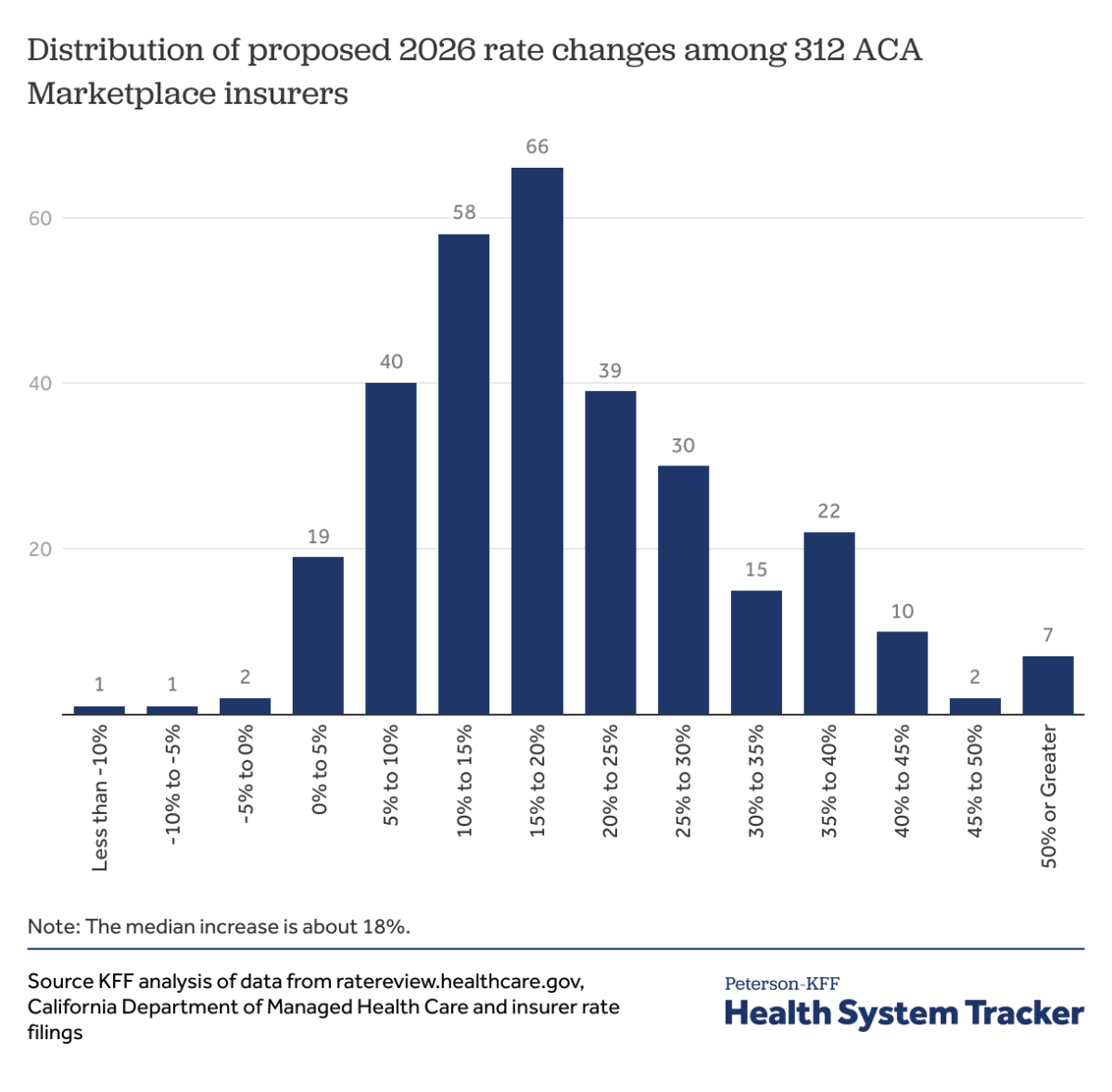

The long post-Affordable Care Act era of moderate health care cost growth may well be ending.

Over the last 15 years, the share of the economy taken up by health care barely budged at all, holding at a little over 17% of GDP. Holding the line for that long is unprecedented and cumulatively saved the taxpayers and premium-payers trillions of dollars over that span. Back in 1996, it took a breadwinner 83 hours of work to earn enough to pay their family's portion of an employer health premium for the year. By 2010, that figure had ballooned to 138 hours of work. Fast forward more than a decade and again you see the Great Health Care Cost Slowdown--by 2023, it took 136 hours of work to pay that portion of the premium, as relative health care cost growth essentially halted in the ACA era.

But now costs are threatening to resume the pre-ACA jumps, exacerbated by a series of bad policy decisions by the current administration. Needless to say, reversing a decade and a half of unprecedented progress would be bad.

Health Care Costs for Workers Begin to Climb

Over the last 15 years, the share of the economy taken up by health care barely budged at all, holding at a little over 17% of GDP. Holding the line for that long is unprecedented and cumulatively saved the taxpayers and premium-payers trillions of dollars over that span. Back in 1996, it took a breadwinner 83 hours of work to earn enough to pay their family's portion of an employer health premium for the year. By 2010, that figure had ballooned to 138 hours of work. Fast forward more than a decade and again you see the Great Health Care Cost Slowdown--by 2023, it took 136 hours of work to pay that portion of the premium, as relative health care cost growth essentially halted in the ACA era.

But now costs are threatening to resume the pre-ACA jumps, exacerbated by a series of bad policy decisions by the current administration. Needless to say, reversing a decade and a half of unprecedented progress would be bad.

Health Care Costs for Workers Begin to Climb

Employees of large and small companies are likely to face higher health care costs, with increases in premiums, bigger deductibles or co-pays, and will possibly lose some benefits next year, according to a large survey of companies nationwide that was released on Thursday.

The survey of 1,700 companies, conducted by Mercer, a benefits consultant, indicated that employers are anticipating the sharpest increases in medical costs in about 15 years. Higher drug costs, rising hospital prices and greater demand for care are all contributing factors, experts said.

Benefit experts say the rising costs are the result of numerous factors, including higher labor costs for health care workers and the introduction of expensive new treatments, including pricey weight-loss drugs. Prescription drug costs are increasingly a concern, with a lot of the blame placed on both the drug manufacturers and the middlemen overseeing drug benefits, the pharmacy benefit managers, for keeping prices high. . . Roughly a third of the overall increase is the result of higher prices charged by hospitals, doctors and other providers, he said.

It is likely to get worse

A series of economic and policy changes will affect many health care sectors.

For one, President Trump’s decision to impose tariffs on imports from many countries could eventually increase the price of drugs and medical supplies, because much of the supply chain begins overseas and those items are largely produced in other nations.

Policy changes related to health care under the Trump administration and the Republican-controlled Congress could drop millions of Americans from Medicaid or subsidized Obamacare insurance, driving up costs for hospitals and other providers. They in turn often try to recoup losses indirectly by charging employer plans at higher rates.

“As hospitals and providers see more uninsured, we always worry that those costs will be absorbed in the system and passed along in terms of higher commercial prices,” said Don Moulds, the chief health director for CalPERS, which offers health benefits to state and local employees in California.