That is correct. For example, this person obviously means “six month

stock of oil.”

But, again, you miss my point entirely. In my

Simplified Exposition of Axiomatic Economics, I write:

The time unit is important because

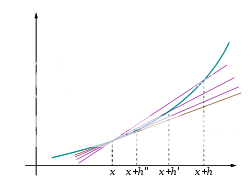

the differentials do not converge to the derivative. Economists use calculus freely, slavishly imitating engineers as though supply were just like velocity, but they do not have convergence. Doing calculus without convergence is like driving a car without a transmission.

For example, if the vertical axis were distance and the horizontal axis were time, then the graph above could represent the position of a golf ball and the slope of the tangent line its velocity. Where the graph is steep, the ball is quickly changing its position, that is, it has a high velocity.

If one wished to measure the ball's current velocity, one could take a picture of it now and then take another picture ten seconds later. The difference in position divided by ten is a measure of the particle's velocity. But it is a coarse measure of the ball's current velocity, as a lot may change before the second picture is taken.

A better measure of the ball's current velocity is to take a picture of it now and then take another picture one second later. Better yet, a video camera could be used which takes pictures every 30th of a second. With flash photography we can obtain quite fine accuracy, as with the photo below, but there is always

some time delay before the second picture is taken. There is no “velocity meter” that gives us the current (instantaneous) velocity the way a camera gives us the current position.

How do we know where the ball was between photos? Intuition tells us that the ball was in points of space between where it was seen, but it may have darted off on a side journey, disappeared entirely or perhaps appeared momentarily on the dark side of the moon before re-joining our intrepid photographer.

We just don't know where the ball was between photographs. It is an axiom of physics that energy and momentum are both conserved.

It is not a result. Darting off on side journeys would violate these conservation principles. Physicists are just not prepared to forsake these long-held axioms because someone raises impertinent questions about where a golf ball was between photos. Brushing impertinent questions aside is the whole point of having axioms. If physics were not based on the axiomatic method, it would degenerate into a skittish empirical science like Post-Autistic Economics, where everybody has an opinion, just like everybody has an _______.

Supply is the economic version of velocity and economists do not have a “supply meter” any more than physicists have a “velocity meter.”

If one wished to measure a factory's current (instantaneous) output, one could take a count of their inventory now and then take another a year later and subtract sales to learn how many widgets they are supplying. But it is a coarse measure of the factory's current output, as a lot may change before the second count is taken. A better measure of the factory's current output is to take a count of the inventory now and then take another a month later. Better yet, one might do this every week, every day or even every hour.

But are these measures of supply really “better” in any sense? They do not converge. The hourly figures would be all over the chart depending on whether the experiment was conducted in the daytime or at night, while the machines were running smoothly or wracked by malfunctions, etc.. Prices exist at every instant, so let us take our instant to be 3:00 a.m. on Sunday morning. A price for widgets exists at this moment, for one can certainly go online and order one. But if economists had established an hour to be their time unit, when they went to construct their supply and demand curves, they would find that supply everywhere is zero. There are no factories running.

So what should the time unit be? A week? A month? It has got to be one or the other and they produce different results. And the different results obtained by different time units do not converge to anything. There is no axiom in Neoclassical Economics equivalent to the conservation principles of physics that assures convergence.

Clearly, there can only be one price and it is not dependent on the caprice of an economist when he decides how often to conduct his surveys any more than the velocity of a golf ball is dependent on how many frames per second the video camera I have purchased operates at. If my camera operates at 30 frames per second and yours at 24 frames per second and we stand side-by-side filming a golf ball sailing past us, we should report close to the same velocity. All of Neoclassical Economics will fall like the House of Usher if it is seen that the prices and quantities it predicts depend entirely on a parameter plucked out of thin air and not on actual market forces.

")

The thread concerns Robert Murphy's challenge to Paul Krugman. Please do not go off on tangents to turn the thread into a personal critique of a fellow DP member.

The thread concerns Robert Murphy's challenge to Paul Krugman. Please do not go off on tangents to turn the thread into a personal critique of a fellow DP member.